Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

Loading...

curl --location 'http://localhost:8082/program-service/v1/program/_create' \

--header 'Content-Type: application/json' \

--data-raw '{

"signature": null,

"header": {

"message_id": "123",

"message_ts": "1708428280",

"message_type": "program",

"action": "create",

"sender_id": "program@https://unified-dev.digit.org",

"receiver_id": "program@https://unified-qa.digit.org"

},

"message": {

"location_code": "pg.citya",

"name": "ifix",

"description": "Empowering local communities through sustainable development projects.",

"start_date": 1672531200,

"end_date": 1704067200,

"children":null,

"status": {

"status_code": "INITIATED",

"status_message": "ACTIVE"

},

"additional_details": {},

"function_code": "in.pg.OGES",

"administration_code": "in.pg.ac.HUDD.UID",

"recipient_segment_code": "in.pg.rsc",

"economic_segment_code": "in.pg.CE.IA.OC",

"source_of_fund_code": "in.pg.CSS",

"target_segment_code": null,

"currency_code": "INR",

"locale_code": "in.pg.citya"

}

}'digit-exchange:develop-1b9d9a2-23program-service:develop-92a135f-55ifms-adapter:develop-bd05fc83-113

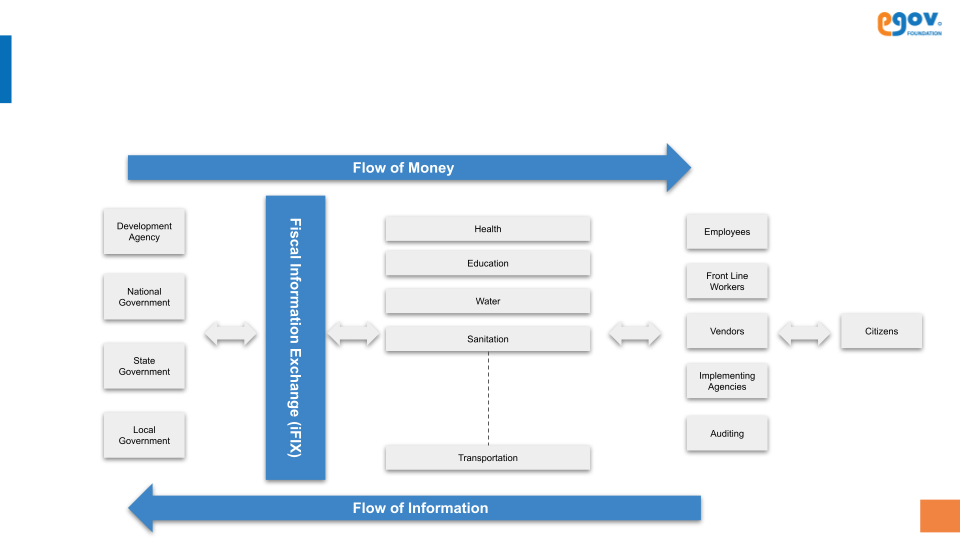

mukta-ifix-adapter:develop-4799181a-46Solution design principles

Technology tools used for the solution design

iFix Infra Setup & Deployment

Core service configuration and promotion docs

Follow our blog section to get insights on public finance management systems, innovations, and impact.

Solution design architecture

Check out the coverage of news and events linked to the PFM platform

iFIX specification details

HeadOfAccounts"HeadOfAccounts": [

{

"id": "1",

"code": "221705800358641045908",

"name": "General Head",

"sequence": 1,

"schemeCode": 13145,

"active": true,

"effectiveFrom": 1682164954037,

"effectiveTo": null

},

]SSUDetails"SSUDetails": [

{

"id": "1",

"ssuCode": "OLSHUD001",

"ddoCode": "OLSHUD001",

"granteeAgCode": "GOHUDULBMPL0036",

"granteeName": "ANGUL MUNICIPALITY",

"programCode": "PG/2023-24/000310",

"ssuId": "1621",

"ssuOffice": "angul_op",

"effectiveFrom": 1682164954037,

"effectiveTo": null,

"active": true

}

]

aws eks update-kubeconfig --region ap-south-1 --name $CLUSTER_NAMEkubectl get svc nginx-ingress-controller -n egov -o jsonpath='{.status.loadBalancer.ingress[0].hostname}'export KUBE_EDITOR='code --wait'

kubectl edit deployment egov-filestore -n egov

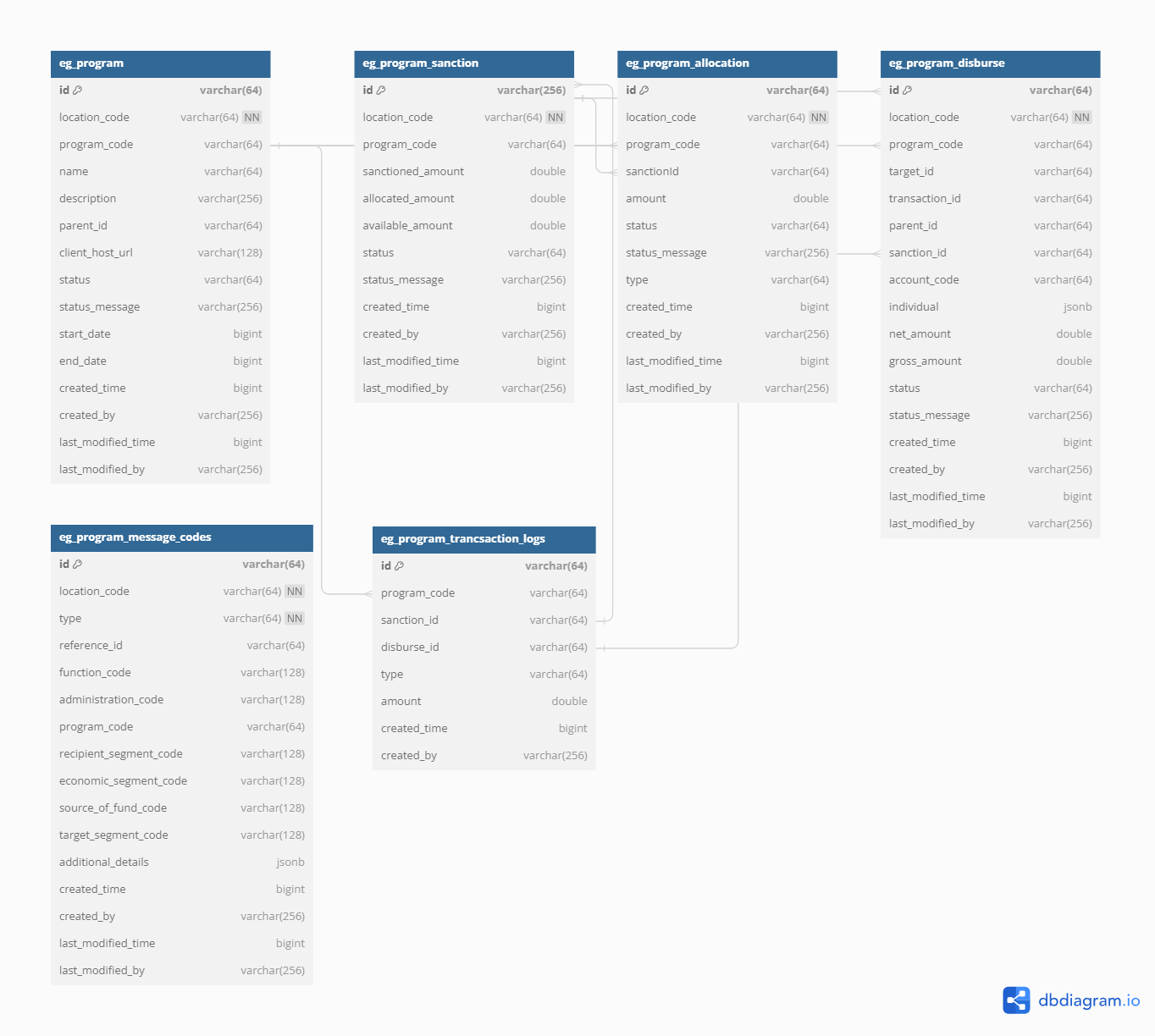

Enables exchange of program, on-program, sanction, on-sanction etc

Signature of {header}+{message} body verified using sender's signing public key

TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==123program@https://spp.example.orghttps://spp.example.org/{namespace}/callback/on-createreceiver id registered with the calling system. Used for authorization, encryption, digital sign verfication, etc., functions.

program@https://pymts.example.orgIs message encrypted?

false{"location_code":"pg.citya","name":"Test 1","start_date":0,"end_date":0,"client_host_url":"https://unified-dev.digit.org","function_code":"string","administration_code":"string","recipient_segment_code":"string","economic_segment_code":"string","source_of_fund_code":"string","target_segment_code":"string","currency_code":"string","locale_code":"string","status":{"status_code":"RECEIVED","status_message":"string"}}HTTP layer error details

HTTP transport layer error codes. Used by components like gateways, LB responding with HTTP status codes 1xx, 2xx, 3xx, 4xx and 5xx

HTTP layer error details

HTTP layer error details

Acknowledgement of message received after successful validation of message and signature

POST /digit-exchange/v1/exchange/EXCHANGE_TYPE HTTP/1.1

Content-Type: application/json

Accept: */*

Content-Length: 1107

{

"signature": "TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==",

"header": {

"message_id": "123",

"message_ts": "text",

"action": "create",

"sender_id": "program@https://spp.example.org",

"sender_uri": "https://spp.example.org/{namespace}/callback/on-create",

"receiver_id": "program@https://pymts.example.org",

"is_msg_encrypted": false

},

"message": "{\"location_code\":\"pg.citya\",\"name\":\"Test 1\",\"start_date\":0,\"end_date\":0,\"client_host_url\":\"https://unified-dev.digit.org\",\"function_code\":\"string\",\"administration_code\":\"string\",\"recipient_segment_code\":\"string\",\"economic_segment_code\":\"string\",\"source_of_fund_code\":\"string\",\"target_segment_code\":\"string\",\"currency_code\":\"string\",\"locale_code\":\"string\",\"status\":{\"status_code\":\"RECEIVED\",\"status_message\":\"string\"}}"

}

{

"errors": [

{

"code": "text",

"message": "text"

}

]

}Create programs in the system

Signature of {header}+{message} body verified using sender's signing public key

TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==251c51eb-e970-4e01-a99a-70136c47a9341708428280ifix@https://mukta.odisa.govt.orghttps://mukta.odisa.govt.org/{namespace}/callback/on-searchreceiver id registered with the calling system. Used for authorization, encryption, digital sign verfication, etc., functions.

ifix@https://ifms.odisa.govt.org251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, Delhi251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, DelhiSUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007SUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007HTTP layer error details

HTTP transport layer error codes. Used by components like gateways, LB responding with HTTP status codes 1xx, 2xx, 3xx, 4xx and 5xx

HTTP layer error details

HTTP layer error details

Acknowledgement of message received after successful validation of message and signature

Enables exchange of program related messages

Signature of {header}+{message} body verified using sender's signing public key

TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==251c51eb-e970-4e01-a99a-70136c47a9341708428280updateifix@https://mukta.odisa.govt.orghttps://mukta.odisa.govt.org/{namespace}/callback/on-searchreceiver id registered with the calling system. Used for authorization, encryption, digital sign verfication, etc., functions.

ifix@https://ifms.odisa.govt.org251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, Delhi251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, DelhiSUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007SUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007HTTP layer error details

HTTP transport layer error codes. Used by components like gateways, LB responding with HTTP status codes 1xx, 2xx, 3xx, 4xx and 5xx

HTTP layer error details

HTTP layer error details

Acknowledgement of message received after successful validation of message and signature

Creates estimate for the program.

Signature of {header}+{message} body verified using sender's signing public key

TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==251c51eb-e970-4e01-a99a-70136c47a9341708428280ifix@https://mukta.odisa.govt.orghttps://mukta.odisa.govt.org/{namespace}/callback/on-searchreceiver id registered with the calling system. Used for authorization, encryption, digital sign verfication, etc., functions.

ifix@https://ifms.odisa.govt.org251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, Delhi251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, DelhiSUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007SUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007HTTP layer error details

HTTP transport layer error codes. Used by components like gateways, LB responding with HTTP status codes 1xx, 2xx, 3xx, 4xx and 5xx

HTTP layer error details

HTTP layer error details

Acknowledgement of message received after successful validation of message and signature

User can update the estimate if already created using on-estimate.

Signature of {header}+{message} body verified using sender's signing public key

TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==251c51eb-e970-4e01-a99a-70136c47a9341708428280createifix@https://mukta.odisa.govt.orghttps://mukta.odisa.govt.org/{namespace}/callback/on-searchreceiver id registered with the calling system. Used for authorization, encryption, digital sign verfication, etc., functions.

ifix@https://ifms.odisa.govt.org251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, Delhi251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, DelhiSUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007SUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007HTTP layer error details

HTTP transport layer error codes. Used by components like gateways, LB responding with HTTP status codes 1xx, 2xx, 3xx, 4xx and 5xx

HTTP layer error details

HTTP layer error details

Acknowledgement of message received after successful validation of message and signature

Create sanction request in the system, this sanction is linked with program.

Signature of {header}+{message} body verified using sender's signing public key

TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==251c51eb-e970-4e01-a99a-70136c47a9341708428280createifix@https://mukta.odisa.govt.orghttps://mukta.odisa.govt.org/{namespace}/callback/on-searchreceiver id registered with the calling system. Used for authorization, encryption, digital sign verfication, etc., functions.

ifix@https://ifms.odisa.govt.org251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, Delhi251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, DelhiSUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007SUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007HTTP layer error details

HTTP transport layer error codes. Used by components like gateways, LB responding with HTTP status codes 1xx, 2xx, 3xx, 4xx and 5xx

HTTP layer error details

HTTP layer error details

Acknowledgement of message received after successful validation of message and signature

Update staus of created sanciton request.

Signature of {header}+{message} body verified using sender's signing public key

TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==251c51eb-e970-4e01-a99a-70136c47a9341708428280updateifix@https://mukta.odisa.govt.orghttps://mukta.odisa.govt.org/{namespace}/callback/on-searchreceiver id registered with the calling system. Used for authorization, encryption, digital sign verfication, etc., functions.

ifix@https://ifms.odisa.govt.org251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, Delhi251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, DelhiSUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007SUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007HTTP layer error details

HTTP transport layer error codes. Used by components like gateways, LB responding with HTTP status codes 1xx, 2xx, 3xx, 4xx and 5xx

HTTP layer error details

HTTP layer error details

Acknowledgement of message received after successful validation of message and signature

User can request to create an allocation for sanction.

Signature of {header}+{message} body verified using sender's signing public key

TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==251c51eb-e970-4e01-a99a-70136c47a9341708428280createifix@https://mukta.odisa.govt.orghttps://mukta.odisa.govt.org/{namespace}/callback/on-searchreceiver id registered with the calling system. Used for authorization, encryption, digital sign verfication, etc., functions.

ifix@https://ifms.odisa.govt.org251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, Delhi251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, DelhiSUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007SUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007HTTP layer error details

HTTP transport layer error codes. Used by components like gateways, LB responding with HTTP status codes 1xx, 2xx, 3xx, 4xx and 5xx

HTTP layer error details

HTTP layer error details

Acknowledgement of message received after successful validation of message and signature

Update created allocation staus

Signature of {header}+{message} body verified using sender's signing public key

TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==251c51eb-e970-4e01-a99a-70136c47a9341708428280createifix@https://mukta.odisa.govt.orghttps://mukta.odisa.govt.org/{namespace}/callback/on-searchreceiver id registered with the calling system. Used for authorization, encryption, digital sign verfication, etc., functions.

ifix@https://ifms.odisa.govt.org251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, Delhi251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, DelhiSUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007SUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007HTTP layer error details

HTTP transport layer error codes. Used by components like gateways, LB responding with HTTP status codes 1xx, 2xx, 3xx, 4xx and 5xx

HTTP layer error details

HTTP layer error details

Acknowledgement of message received after successful validation of message and signature

Create new disbursement request to initiate payment.

Signature of {header}+{message} body verified using sender's signing public key

TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==251c51eb-e970-4e01-a99a-70136c47a9341708428280createifix@https://mukta.odisa.govt.orghttps://mukta.odisa.govt.org/{namespace}/callback/on-searchreceiver id registered with the calling system. Used for authorization, encryption, digital sign verfication, etc., functions.

ifix@https://ifms.odisa.govt.org251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, Delhi251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, DelhiSUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007SUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007HTTP layer error details

HTTP transport layer error codes. Used by components like gateways, LB responding with HTTP status codes 1xx, 2xx, 3xx, 4xx and 5xx

HTTP layer error details

HTTP layer error details

Acknowledgement of message received after successful validation of message and signature

Updated status of create disburse request

Signature of {header}+{message} body verified using sender's signing public key

TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==251c51eb-e970-4e01-a99a-70136c47a9341708428280updateifix@https://mukta.odisa.govt.orghttps://mukta.odisa.govt.org/{namespace}/callback/on-searchreceiver id registered with the calling system. Used for authorization, encryption, digital sign verfication, etc., functions.

ifix@https://ifms.odisa.govt.org251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, Delhi251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, DelhiSUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007SUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007HTTP layer error details

HTTP transport layer error codes. Used by components like gateways, LB responding with HTTP status codes 1xx, 2xx, 3xx, 4xx and 5xx

HTTP layer error details

HTTP layer error details

Acknowledgement of message received after successful validation of message and signature

Create new demand request.

Signature of {header}+{message} body verified using sender's signing public key

TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==251c51eb-e970-4e01-a99a-70136c47a9341708428280createifix@https://mukta.odisa.govt.orghttps://mukta.odisa.govt.org/{namespace}/callback/on-searchreceiver id registered with the calling system. Used for authorization, encryption, digital sign verfication, etc., functions.

ifix@https://ifms.odisa.govt.org251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, Delhi251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, DelhiSUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007SUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007HTTP layer error details

HTTP transport layer error codes. Used by components like gateways, LB responding with HTTP status codes 1xx, 2xx, 3xx, 4xx and 5xx

HTTP layer error details

HTTP layer error details

Acknowledgement of message received after successful validation of message and signature

Updated create demand request

Signature of {header}+{message} body verified using sender's signing public key

TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==251c51eb-e970-4e01-a99a-70136c47a9341708428280updateifix@https://mukta.odisa.govt.orghttps://mukta.odisa.govt.org/{namespace}/callback/on-searchreceiver id registered with the calling system. Used for authorization, encryption, digital sign verfication, etc., functions.

ifix@https://ifms.odisa.govt.org251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, Delhi251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, DelhiSUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007SUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007HTTP layer error details

HTTP transport layer error codes. Used by components like gateways, LB responding with HTTP status codes 1xx, 2xx, 3xx, 4xx and 5xx

HTTP layer error details

HTTP layer error details

Acknowledgement of message received after successful validation of message and signature

Create new receipt.

Signature of {header}+{message} body verified using sender's signing public key

TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==251c51eb-e970-4e01-a99a-70136c47a9341708428280createifix@https://mukta.odisa.govt.orghttps://mukta.odisa.govt.org/{namespace}/callback/on-searchreceiver id registered with the calling system. Used for authorization, encryption, digital sign verfication, etc., functions.

ifix@https://ifms.odisa.govt.org251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, Delhi251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, DelhiSUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007SUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007HTTP layer error details

HTTP transport layer error codes. Used by components like gateways, LB responding with HTTP status codes 1xx, 2xx, 3xx, 4xx and 5xx

HTTP layer error details

HTTP layer error details

Acknowledgement of message received after successful validation of message and signature

Updated status of create receipt request

Signature of {header}+{message} body verified using sender's signing public key

TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==251c51eb-e970-4e01-a99a-70136c47a9341708428280updateifix@https://mukta.odisa.govt.orghttps://mukta.odisa.govt.org/{namespace}/callback/on-searchreceiver id registered with the calling system. Used for authorization, encryption, digital sign verfication, etc., functions.

ifix@https://ifms.odisa.govt.org251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, Delhi251c51eb-e970-4e01-a99a-70136c47a934Name of the program

Community Development InitiativeLinked id of the event, if event is dependent on any other. It will be in format {event_type}:uuid

sanction:251c51eb-e970-4e01-a99a-70136c47a934Unique identifier of the tenant that could be a department/ulb/state

pb.jalandharFormated program code PROG/{FINANCIAL_YEAR}/{AUTO_NUMBER}

PORG/2023-24/00001Formated transaction code, it will return after transaction is created in payment system.

PI/2023-24/00001Amount to be paid including deduction amount

1000Actual amount to be paid without deduction

1000John[email protected]98765432101100013476, Gali Bajrang Bali, DelhiSUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007SUCCESSFULPossible values: Additional JSON property oject to hold custom user defined contextual data

username (preferred) or userid of the user that created the object

username (preferred) or userid of the user that last modified the object

epoch of the time object is created

epoch of the time object is last modified

Account no with ifsc code will be account code, it will be in format ACCOUNT_NO@IFSC_CODE

1234567890@SBIN0003491LIVELIHOODHUDDWhoese getting the money

CBOPEOPLESTATEMALEINRLC007HTTP layer error details

HTTP transport layer error codes. Used by components like gateways, LB responding with HTTP status codes 1xx, 2xx, 3xx, 4xx and 5xx

HTTP layer error details

HTTP layer error details

Acknowledgement of message received after successful validation of message and signature

{

"errors": [

{

"code": "text",

"message": "text"

}

]

}{

"errors": [

{

"code": "text",

"message": "text"

}

]

}{

"errors": [

{

"code": "text",

"message": "text"

}

]

}{

"errors": [

{

"code": "text",

"message": "text"

}

]

}{

"errors": [

{

"code": "text",

"message": "text"

}

]

}{

"errors": [

{

"code": "text",

"message": "text"

}

]

}{

"errors": [

{

"code": "text",

"message": "text"

}

]

}{

"errors": [

{

"code": "text",

"message": "text"

}

]

}{

"errors": [

{

"code": "text",

"message": "text"

}

]

}{

"errors": [

{

"code": "text",

"message": "text"

}

]

}{

"errors": [

{

"code": "text",

"message": "text"

}

]

}{

"errors": [

{

"code": "text",

"message": "text"

}

]

}{

"errors": [

{

"code": "text",

"message": "text"

}

]

}{

"errors": [

{

"code": "text",

"message": "text"

}

]

}POST /ifix/v1/program HTTP/1.1

Content-Type: application/json

Accept: */*

Content-Length: 2882

{

"signature": "TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==",

"header": {

"message_id": "251c51eb-e970-4e01-a99a-70136c47a934",

"message_ts": 1708428280,

"action": "create",

"sender_id": "ifix@https://mukta.odisa.govt.org",

"sender_uri": "https://mukta.odisa.govt.org/{namespace}/callback/on-search",

"receiver_id": "ifix@https://ifms.odisa.govt.org"

},

"message": {

"name": "Community Development Initiative",

"linked_id": "sanction:251c51eb-e970-4e01-a99a-70136c47a934",

"location_code": "pb.jalandhar",

"program_code": "PORG/2023-24/00001",

"transaction_id": "PI/2023-24/00001",

"net_amount": 1000,

"gross_amount": 1000,

"individual": {

"name": "John",

"email": "[email protected]",

"phone": 9876543210,

"pin": 110001,

"address": "3476, Gali Bajrang Bali, Delhi"

},

"children": [

{

"name": "Community Development Initiative",

"linked_id": "sanction:251c51eb-e970-4e01-a99a-70136c47a934",

"location_code": "pb.jalandhar",

"program_code": "PORG/2023-24/00001",

"transaction_id": "PI/2023-24/00001",

"net_amount": 1000,

"gross_amount": 1000,

"individual": {

"name": "John",

"email": "[email protected]",

"phone": 9876543210,

"pin": 110001,

"address": "3476, Gali Bajrang Bali, Delhi"

},

"children": [

{

"name": "Community Development Initiative",

"linked_id": "sanction:251c51eb-e970-4e01-a99a-70136c47a934",

"location_code": "pb.jalandhar",

"program_code": "PORG/2023-24/00001",

"transaction_id": "PI/2023-24/00001",

"net_amount": 1000,

"gross_amount": 1000,

"individual": {

"name": "John",

"email": "[email protected]",

"phone": 9876543210,

"pin": 110001,

"address": "3476, Gali Bajrang Bali, Delhi"

},

"children": "[Circular Reference]",

"status": {

"status_code": "SUCCESSFUL",

"status_message": "text"

},

"additional_details": {},

"account_code": "1234567890@SBIN0003491",

"function_code": "LIVELIHOOD",

"administration_code": "HUDD",

"recipient_segment_code": "CBO",

"economic_segment_code": "PEOPLE",

"source_of_fund_code": "STATE",

"target_segment_code": "MALE",

"currency_code": "INR",

"locale_code": "LC007"

}

],

"status": {

"status_code": "SUCCESSFUL",

"status_message": "text"

},

"additional_details": {},

"account_code": "1234567890@SBIN0003491",

"function_code": "LIVELIHOOD",

"administration_code": "HUDD",

"recipient_segment_code": "CBO",

"economic_segment_code": "PEOPLE",

"source_of_fund_code": "STATE",

"target_segment_code": "MALE",

"currency_code": "INR",

"locale_code": "LC007"

}

],

"status": {

"status_code": "SUCCESSFUL",

"status_message": "text"

},

"additional_details": {},

"account_code": "1234567890@SBIN0003491",

"function_code": "LIVELIHOOD",

"administration_code": "HUDD",

"recipient_segment_code": "CBO",

"economic_segment_code": "PEOPLE",

"source_of_fund_code": "STATE",

"target_segment_code": "MALE",

"currency_code": "INR",

"locale_code": "LC007"

}

}POST /ifix/v1/on-program HTTP/1.1

Content-Type: application/json

Accept: */*

Content-Length: 2146

{

"signature": "TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==",

"header": {

"message_id": "251c51eb-e970-4e01-a99a-70136c47a934",

"message_ts": 1708428280,

"action": "update",

"sender_id": "ifix@https://mukta.odisa.govt.org",

"sender_uri": "https://mukta.odisa.govt.org/{namespace}/callback/on-search",

"receiver_id": "ifix@https://ifms.odisa.govt.org"

},

"message": {

"name": "Community Development Initiative",

"linked_id": "sanction:251c51eb-e970-4e01-a99a-70136c47a934",

"location_code": "pb.jalandhar",

"program_code": "PORG/2023-24/00001",

"transaction_id": "PI/2023-24/00001",

"net_amount": 1000,

"gross_amount": 1000,

"individual": {

"name": "John",

"email": "[email protected]",

"phone": 9876543210,

"pin": 110001,

"address": "3476, Gali Bajrang Bali, Delhi"

},

"children": [

{

"name": "Community Development Initiative",

"linked_id": "sanction:251c51eb-e970-4e01-a99a-70136c47a934",

"location_code": "pb.jalandhar",

"program_code": "PORG/2023-24/00001",

"transaction_id": "PI/2023-24/00001",

"net_amount": 1000,

"gross_amount": 1000,

"individual": {

"name": "John",

"email": "[email protected]",

"phone": 9876543210,

"pin": 110001,

"address": "3476, Gali Bajrang Bali, Delhi"

},

"children": [

"[Circular Reference]"

],

"status": {

"status_code": "SUCCESSFUL",

"status_message": "text"

},

"additional_details": {},

"account_code": "1234567890@SBIN0003491",

"function_code": "LIVELIHOOD",

"administration_code": "HUDD",

"recipient_segment_code": "CBO",

"economic_segment_code": "PEOPLE",

"source_of_fund_code": "STATE",

"target_segment_code": "MALE",

"currency_code": "INR",

"locale_code": "LC007"

}

],

"status": {

"status_code": "SUCCESSFUL",

"status_message": "text"

},

"additional_details": {},

"account_code": "1234567890@SBIN0003491",

"function_code": "LIVELIHOOD",

"administration_code": "HUDD",

"recipient_segment_code": "CBO",

"economic_segment_code": "PEOPLE",

"source_of_fund_code": "STATE",

"target_segment_code": "MALE",

"currency_code": "INR",

"locale_code": "LC007"

}

}POST /ifix/v1/estimate HTTP/1.1

Content-Type: application/json

Accept: */*

Content-Length: 2882

{

"signature": "TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==",

"header": {

"message_id": "251c51eb-e970-4e01-a99a-70136c47a934",

"message_ts": 1708428280,

"action": "create",

"sender_id": "ifix@https://mukta.odisa.govt.org",

"sender_uri": "https://mukta.odisa.govt.org/{namespace}/callback/on-search",

"receiver_id": "ifix@https://ifms.odisa.govt.org"

},

"message": {

"name": "Community Development Initiative",

"linked_id": "sanction:251c51eb-e970-4e01-a99a-70136c47a934",

"location_code": "pb.jalandhar",

"program_code": "PORG/2023-24/00001",

"transaction_id": "PI/2023-24/00001",

"net_amount": 1000,

"gross_amount": 1000,

"individual": {

"name": "John",

"email": "[email protected]",

"phone": 9876543210,

"pin": 110001,

"address": "3476, Gali Bajrang Bali, Delhi"

},

"children": [

{

"name": "Community Development Initiative",

"linked_id": "sanction:251c51eb-e970-4e01-a99a-70136c47a934",

"location_code": "pb.jalandhar",

"program_code": "PORG/2023-24/00001",

"transaction_id": "PI/2023-24/00001",

"net_amount": 1000,

"gross_amount": 1000,

"individual": {

"name": "John",

"email": "[email protected]",

"phone": 9876543210,

"pin": 110001,

"address": "3476, Gali Bajrang Bali, Delhi"

},

"children": [

{

"name": "Community Development Initiative",

"linked_id": "sanction:251c51eb-e970-4e01-a99a-70136c47a934",

"location_code": "pb.jalandhar",

"program_code": "PORG/2023-24/00001",

"transaction_id": "PI/2023-24/00001",

"net_amount": 1000,

"gross_amount": 1000,

"individual": {

"name": "John",

"email": "[email protected]",

"phone": 9876543210,

"pin": 110001,

"address": "3476, Gali Bajrang Bali, Delhi"

},

"children": "[Circular Reference]",

"status": {

"status_code": "SUCCESSFUL",

"status_message": "text"

},

"additional_details": {},

"account_code": "1234567890@SBIN0003491",

"function_code": "LIVELIHOOD",

"administration_code": "HUDD",

"recipient_segment_code": "CBO",

"economic_segment_code": "PEOPLE",

"source_of_fund_code": "STATE",

"target_segment_code": "MALE",

"currency_code": "INR",

"locale_code": "LC007"

}

],

"status": {

"status_code": "SUCCESSFUL",

"status_message": "text"

},

"additional_details": {},

"account_code": "1234567890@SBIN0003491",

"function_code": "LIVELIHOOD",

"administration_code": "HUDD",

"recipient_segment_code": "CBO",

"economic_segment_code": "PEOPLE",

"source_of_fund_code": "STATE",

"target_segment_code": "MALE",

"currency_code": "INR",

"locale_code": "LC007"

}

],

"status": {

"status_code": "SUCCESSFUL",

"status_message": "text"

},

"additional_details": {},

"account_code": "1234567890@SBIN0003491",

"function_code": "LIVELIHOOD",

"administration_code": "HUDD",

"recipient_segment_code": "CBO",

"economic_segment_code": "PEOPLE",

"source_of_fund_code": "STATE",

"target_segment_code": "MALE",

"currency_code": "INR",

"locale_code": "LC007"

}

}POST /ifix/v1/on-estimate HTTP/1.1

Content-Type: application/json

Accept: */*

Content-Length: 2882

{

"signature": "TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==",

"header": {

"message_id": "251c51eb-e970-4e01-a99a-70136c47a934",

"message_ts": 1708428280,

"action": "create",

"sender_id": "ifix@https://mukta.odisa.govt.org",

"sender_uri": "https://mukta.odisa.govt.org/{namespace}/callback/on-search",

"receiver_id": "ifix@https://ifms.odisa.govt.org"

},

"message": {

"name": "Community Development Initiative",

"linked_id": "sanction:251c51eb-e970-4e01-a99a-70136c47a934",

"location_code": "pb.jalandhar",

"program_code": "PORG/2023-24/00001",

"transaction_id": "PI/2023-24/00001",

"net_amount": 1000,

"gross_amount": 1000,

"individual": {

"name": "John",

"email": "[email protected]",

"phone": 9876543210,

"pin": 110001,

"address": "3476, Gali Bajrang Bali, Delhi"

},

"children": [

{

"name": "Community Development Initiative",

"linked_id": "sanction:251c51eb-e970-4e01-a99a-70136c47a934",

"location_code": "pb.jalandhar",

"program_code": "PORG/2023-24/00001",

"transaction_id": "PI/2023-24/00001",

"net_amount": 1000,

"gross_amount": 1000,

"individual": {

"name": "John",

"email": "[email protected]",

"phone": 9876543210,

"pin": 110001,

"address": "3476, Gali Bajrang Bali, Delhi"

},

"children": [

{

"name": "Community Development Initiative",

"linked_id": "sanction:251c51eb-e970-4e01-a99a-70136c47a934",

"location_code": "pb.jalandhar",

"program_code": "PORG/2023-24/00001",

"transaction_id": "PI/2023-24/00001",

"net_amount": 1000,

"gross_amount": 1000,

"individual": {

"name": "John",

"email": "[email protected]",

"phone": 9876543210,

"pin": 110001,

"address": "3476, Gali Bajrang Bali, Delhi"

},

"children": "[Circular Reference]",

"status": {

"status_code": "SUCCESSFUL",

"status_message": "text"

},

"additional_details": {},

"account_code": "1234567890@SBIN0003491",

"function_code": "LIVELIHOOD",

"administration_code": "HUDD",

"recipient_segment_code": "CBO",

"economic_segment_code": "PEOPLE",

"source_of_fund_code": "STATE",

"target_segment_code": "MALE",

"currency_code": "INR",

"locale_code": "LC007"

}

],

"status": {

"status_code": "SUCCESSFUL",

"status_message": "text"

},

"additional_details": {},

"account_code": "1234567890@SBIN0003491",

"function_code": "LIVELIHOOD",

"administration_code": "HUDD",

"recipient_segment_code": "CBO",

"economic_segment_code": "PEOPLE",

"source_of_fund_code": "STATE",

"target_segment_code": "MALE",

"currency_code": "INR",

"locale_code": "LC007"

}

],

"status": {

"status_code": "SUCCESSFUL",

"status_message": "text"

},

"additional_details": {},

"account_code": "1234567890@SBIN0003491",

"function_code": "LIVELIHOOD",

"administration_code": "HUDD",

"recipient_segment_code": "CBO",

"economic_segment_code": "PEOPLE",

"source_of_fund_code": "STATE",

"target_segment_code": "MALE",

"currency_code": "INR",

"locale_code": "LC007"

}

}POST /ifix/v1/sanction HTTP/1.1

Content-Type: application/json

Accept: */*

Content-Length: 2882

{

"signature": "TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==",

"header": {

"message_id": "251c51eb-e970-4e01-a99a-70136c47a934",

"message_ts": 1708428280,

"action": "create",

"sender_id": "ifix@https://mukta.odisa.govt.org",

"sender_uri": "https://mukta.odisa.govt.org/{namespace}/callback/on-search",

"receiver_id": "ifix@https://ifms.odisa.govt.org"

},

"message": {

"name": "Community Development Initiative",

"linked_id": "sanction:251c51eb-e970-4e01-a99a-70136c47a934",

"location_code": "pb.jalandhar",

"program_code": "PORG/2023-24/00001",

"transaction_id": "PI/2023-24/00001",

"net_amount": 1000,

"gross_amount": 1000,

"individual": {

"name": "John",

"email": "[email protected]",

"phone": 9876543210,

"pin": 110001,

"address": "3476, Gali Bajrang Bali, Delhi"

},

"children": [

{

"name": "Community Development Initiative",

"linked_id": "sanction:251c51eb-e970-4e01-a99a-70136c47a934",

"location_code": "pb.jalandhar",

"program_code": "PORG/2023-24/00001",

"transaction_id": "PI/2023-24/00001",

"net_amount": 1000,

"gross_amount": 1000,

"individual": {

"name": "John",

"email": "[email protected]",

"phone": 9876543210,

"pin": 110001,

"address": "3476, Gali Bajrang Bali, Delhi"

},

"children": [

{

"name": "Community Development Initiative",

"linked_id": "sanction:251c51eb-e970-4e01-a99a-70136c47a934",

"location_code": "pb.jalandhar",

"program_code": "PORG/2023-24/00001",

"transaction_id": "PI/2023-24/00001",

"net_amount": 1000,

"gross_amount": 1000,

"individual": {

"name": "John",

"email": "[email protected]",

"phone": 9876543210,

"pin": 110001,

"address": "3476, Gali Bajrang Bali, Delhi"

},

"children": "[Circular Reference]",

"status": {

"status_code": "SUCCESSFUL",

"status_message": "text"

},

"additional_details": {},

"account_code": "1234567890@SBIN0003491",

"function_code": "LIVELIHOOD",

"administration_code": "HUDD",

"recipient_segment_code": "CBO",

"economic_segment_code": "PEOPLE",

"source_of_fund_code": "STATE",

"target_segment_code": "MALE",

"currency_code": "INR",

"locale_code": "LC007"

}

],

"status": {

"status_code": "SUCCESSFUL",

"status_message": "text"

},

"additional_details": {},

"account_code": "1234567890@SBIN0003491",

"function_code": "LIVELIHOOD",

"administration_code": "HUDD",

"recipient_segment_code": "CBO",

"economic_segment_code": "PEOPLE",

"source_of_fund_code": "STATE",

"target_segment_code": "MALE",

"currency_code": "INR",

"locale_code": "LC007"

}

],

"status": {

"status_code": "SUCCESSFUL",

"status_message": "text"

},

"additional_details": {},

"account_code": "1234567890@SBIN0003491",

"function_code": "LIVELIHOOD",

"administration_code": "HUDD",

"recipient_segment_code": "CBO",

"economic_segment_code": "PEOPLE",

"source_of_fund_code": "STATE",

"target_segment_code": "MALE",

"currency_code": "INR",

"locale_code": "LC007"

}

}POST /ifix/v1/on-sanction HTTP/1.1

Content-Type: application/json

Accept: */*

Content-Length: 2882

{

"signature": "TgE1hcA2E+YPMdPGz4vveKQpR0x+pgzRTlet52qh63Kekr71vWWScXqaRFtQW64uRFZGBUhHYYZQ2y6LffwnNOOQhhssaThhqVBhXNEwX9i75SNYXi5XSJVDYzSyHrhF20HW6RE9mAVWdc80i7d+FXlh+b/U+fnj+SrZ2s6Xd0WUZvU29LgqeUpyznlWLu1mDdJxNZavsDLWmxjTnknqBjDvwSc35WhFDhXDA2lWmm8YpZ1Y6TBmvvtVS7mAOTnhFy9sdCbrLcfXk5QWIsdzlvPqlkvdwEf30OZ6ewb680Aj3hO2OT5LCv7iLyz7C7srnB9lJT5gXiw+eSnktPXlDA==",

"header": {

"message_id": "251c51eb-e970-4e01-a99a-70136c47a934",

"message_ts": 1708428280,

"action": "update",

"sender_id": "ifix@https://mukta.odisa.govt.org",

"sender_uri": "https://mukta.odisa.govt.org/{namespace}/callback/on-search",

"receiver_id": "ifix@https://ifms.odisa.govt.org"

},

"message": {

"name": "Community Development Initiative",

"linked_id": "sanction:251c51eb-e970-4e01-a99a-70136c47a934",

"location_code": "pb.jalandhar",

"program_code": "PORG/2023-24/00001",

"transaction_id": "PI/2023-24/00001",

"net_amount": 1000,

"gross_amount": 1000,

"individual": {

"name": "John",

"email": "[email protected]",

"phone": 9876543210,

"pin": 110001,

"address": "3476, Gali Bajrang Bali, Delhi"

},

"children": [

{

"name": "Community Development Initiative",

"linked_id": "sanction:251c51eb-e970-4e01-a99a-70136c47a934",

"location_code": "pb.jalandhar",

"program_code": "PORG/2023-24/00001",

"transaction_id": "PI/2023-24/00001",

"net_amount": 1000,

"gross_amount": 1000,

"individual": {

"name": "John",

"email": "[email protected]",

"phone": 9876543210,

"pin": 110001,

"address": "3476, Gali Bajrang Bali, Delhi"

},

"children": [

{

"name": "Community Development Initiative",

"linked_id": "sanction:251c51eb-e970-4e01-a99a-70136c47a934",

"location_code": "pb.jalandhar",

"program_code": "PORG/2023-24/00001",

"transaction_id": "PI/2023-24/00001",

"net_amount": 1000,

"gross_amount": 1000,

"individual": {

"name": "John",

"email": "[email protected]",

"phone": 9876543210,

"pin": 110001,

"address": "3476, Gali Bajrang Bali, Delhi"

},

"children": "[Circular Reference]",

"status": {

"status_code": "SUCCESSFUL",

"status_message": "text"

},

"additional_details": {},

"account_code": "1234567890@SBIN0003491",

"function_code": "LIVELIHOOD",

"administration_code": "HUDD",

"recipient_segment_code": "CBO",

"economic_segment_code": "PEOPLE",

"source_of_fund_code": "STATE",

"target_segment_code": "MALE",

"currency_code": "INR",

"locale_code": "LC007"

}

],

"status": {

"status_code": "SUCCESSFUL",

"status_message": "text"

},

"additional_details": {},

"account_code": "1234567890@SBIN0003491",

"function_code": "LIVELIHOOD",

"administration_code": "HUDD",

"recipient_segment_code": "CBO",

"economic_segment_code": "PEOPLE",

"source_of_fund_code": "STATE",

"target_segment_code": "MALE",

"currency_code": "INR",

"locale_code": "LC007"

}

],

"status": {

"status_code": "SUCCESSFUL",

"status_message": "text"

},

"additional_details": {},

"account_code": "1234567890@SBIN0003491",

"function_code": "LIVELIHOOD",

"administration_code": "HUDD",